Medicaid Planning vs. Traditional Estate Planning

Medicaid Planning vs. Traditional Estate Planning in Florida: Understanding Key Differences for Asset Protection and Eligibility

By Michelle A Berglund-Harper, Esq., Murphy & Berglund, PLLC

Navigating the complexities of estate planning can be daunting, especially when it comes to understanding the differences between Medicaid planning and traditional estate planning in Florida. This article aims to demystify these two crucial financial strategies, helping you comprehend their distinct roles in asset protection and eligibility for government assistance. By exploring the key differences, we will provide clarity on how these planning methods function to safeguard your wealth and ensure you receive the necessary care without jeopardizing your assets. We will delve into their respective asset protection strategies, eligibility requirements, and implications for individuals. Knowledge in these areas can empower you to make informed decisions that best suit your financial future.

Key Differences:

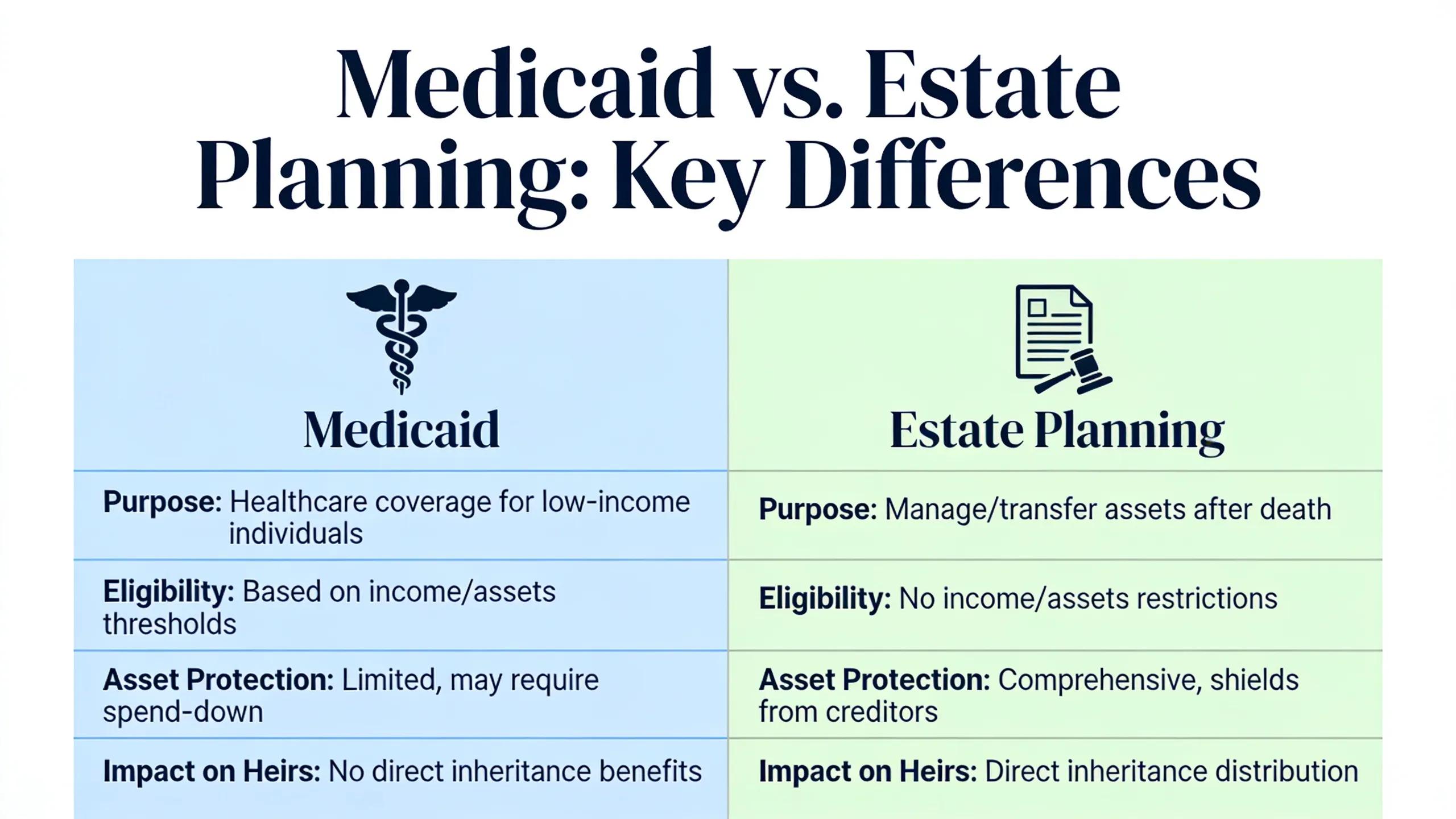

Understanding the key differences between Medicaid planning and traditional estate planning is essential for those looking to protect their assets and prepare for potential healthcare needs. Both approaches serve unique purposes in the financial landscape, with Medicaid planning focusing on eligibility for government benefits and asset preservation for long-term care. Traditional estate planning, on the other hand, primarily addresses the distribution of assets upon death and may not always consider the implications of long-term care needs. Here are some crucial distinctions:

Asset Protection:

Asset protection strategies differ significantly between Medicaid planning and traditional estate planning. Medicaid planning utilizes specific tools and structures to shield assets from exposure to nursing home costs. Strategies such as the establishment of irrevocable trusts can protect assets while allowing individuals to qualify for Medicaid benefits. In contrast, traditional estate planning often involves the use of wills and revocable trusts, which may not effectively protect assets in the event of a nursing home stay.

Eligibility Requirements:

The eligibility requirements for Medicaid are notably stricter than those typically associated with traditional estate planning. For Medicaid in Florida, applicants must demonstrate financial limitations and adhere to the five-year look-back period. This means that any asset transfers made within five years prior to the application may be scrutinized, which could potentially delay or disqualify an applicant. Traditional estate planning does not impose such rigorous financial assessments, focusing more on the disposition of assets upon death.

Implications for Individuals:

The implications of choosing between Medicaid planning and traditional estate planning can significantly affect an individual’s financial wellbeing. Inadequate planning can lead to severe financial consequences, such as the loss of assets due to nursing home costs or inability to secure necessary medical care. Understanding the financial ramifications of each strategy can help individuals make informed decisions that align with their long-term care goals while ensuring their family wealth is preserved.

What Are the Core Differences Between Medicaid Planning and Traditional Estate Planning in Florida?

Medicaid planning and traditional estate planning serve foundationally different purposes, particularly in the context of Florida’s regulatory environment. Medicaid planning primarily focuses on qualifying for long-term care benefits while safeguarding assets from nursing home costs. In contrast, traditional estate planning concentrates on the posthumous distribution of one’s estate, aiming for seamless transitions for heirs. Recognizing these distinctions is crucial for effective financial planning.

How Does Medicaid Planning Address Florida’s Long Term Care Costs?

In Florida, Medicaid planning is a fundamental strategy for managing long-term care costs. As the state has a high demand for elderly services, Medicaid provides crucial assistance in covering costly long-term care. Proper Medicaid planning can ensure that eligible individuals receive care without stripping their families of financial security. This involves navigating income and asset limits that are specific to Florida residents while employing various planning techniques to maximize available resources. For an indepth look at strategies involved with nursing home planning, you can order our book from Amazon or pick up a copy at our office, located in Altamonte Springs, FL.

What Legal Instruments Define Traditional Estate Planning Under Florida Law?

Traditional estate planning in Florida primarily involves the use of legal instruments such as wills and trusts. Wills designate how assets will be distributed upon death, while revocable trusts allow individuals to manage their assets during their lifetime and dictate distribution after death, without the necessity of probate. Additionally, durable powers of attorney and healthcare proxies play significant roles in ensuring that individuals’ wishes regarding medical care and financial management are respected in times of incapacity.

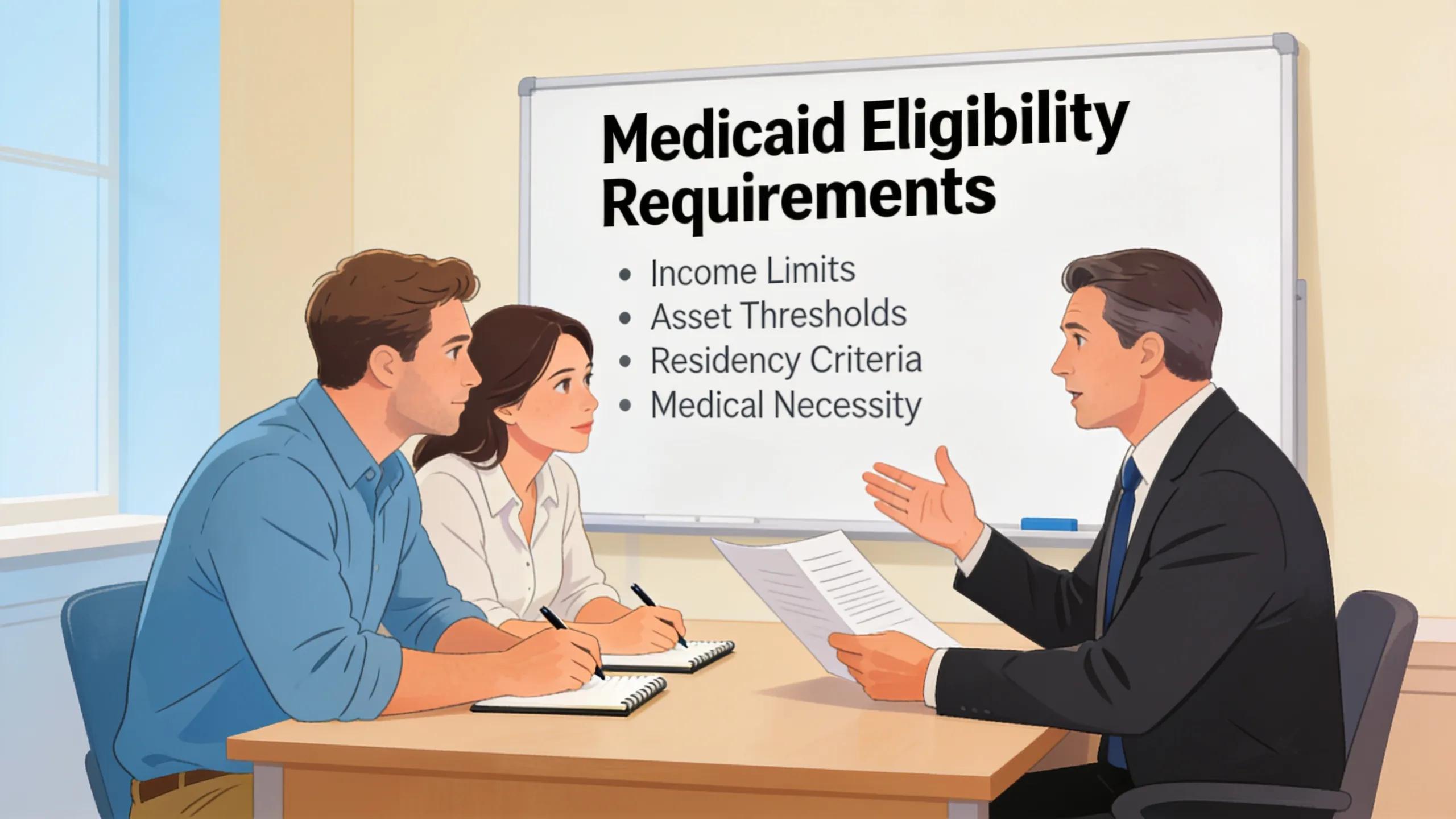

What Are the Medicaid Eligibility Requirements and Their Impact on Planning in Florida?

The Medicaid eligibility requirements in Florida are stringent and can profoundly impact planning efforts. Individuals must meet specific income and asset criteria to qualify for benefits, which includes a thorough examination of assets through a five-year look-back period. This timeframe emphasizes the importance of proactive planning strategies to safeguard assets and ensure eligibility. Failure to adhere to these requirements can result in denied applications or unexpected financial burdens.

Which Asset and Income Limits Govern Medicaid Qualification in Florida?

In Florida, Medicaid qualification is primarily governed by asset and income limits. As of June 2026, an individual must have countable assets below $2,000 to qualify for Medicaid. Furthermore, the monthly income limit for single applicants may not exceed approximately $2,982, although this figure is subject to regular adjustments. Understanding these thresholds is essential for effective Medicaid planning, as they directly influence both eligibility and financial strategy.

How Do Spend-Down and Look-Back Periods Affect Medicaid Asset Protection?

The spend-down process in conjunction with the look-back period significantly affects Medicaid asset protection strategies. During the five-year look-back, any assets transferred or gifted can be subject to penalties, delaying eligibility for benefits. Spend-down strategies can involve specific expenses that reduce countable assets, such as healthcare costs or home improvements, allowing individuals to qualify for Medicaid without losing their essential resources.

How Does Traditional Estate Planning Manage Asset Distribution Differently from Medicaid Planning?

Traditional estate planning and Medicaid planning diverge markedly in their management of asset distribution. While traditional estate planning focuses on the orderly transfer of assets upon death, Medicaid planning prioritizes preserving those assets to qualify for long-term care funding. This divergence necessitates a careful assessment of both strategies to ensure there is no conflict between the goals of asset preservation and the desired distribution to heirs.

What Roles Do Wills and Trusts Play in Florida Estate Planning?

Wills and trusts play pivotal roles in Florida estate planning, each serving unique functions within the overall strategy. Wills primarily direct the distribution of assets posthumously, while trusts can provide ongoing management of assets both during a person’s lifetime and after their death. Trusts can also offer mechanisms for protecting assets from creditors and ensuring specific asset distributions aligned with the grantor’s wishes, particularly important in the context of long-term care planning.

How Does Estate Planning Address Long Term Care and Elder Law Without Medicaid?

Without Medicaid, estate planning addresses long-term care through alternative strategies such as private long-term care insurance or personal savings. While Medicaid provides crucial support, planning for alternative funding sources is essential for those who may not qualify or prefer other options. Estate planning can assist in setting aside funds specifically for medical care while ensuring that individuals retain their desired level of financial security.

What Strategies Protect Assets From Medicaid Costs and Facilitate Effective Long Term Care Planning in Florida?

Several strategies can be employed to protect assets from Medicaid costs while facilitating effective long-term care planning in Florida. One common approach is establishing irrevocable trusts that exclude assets from the individual’s estate, for those folks who are planning early (5+ years away from needing Medicaid Benefits). Other methods include spending down assets on qualified expenses, leveraging annuities, personal service contracts, and utilizing specific exemptions for primary residences or certain types of income. Each strategy requires meticulous planning to ensure compliance with Medicaid regulations while preserving individual financial security.

Which Medicaid Asset Protection Tools Are Recognized Under Florida Law?

Florida law recognizes various Medicaid asset protection tools designed to help individuals qualify for benefits while safeguarding their wealth. Common tools include irrevocable trusts, prepaid funeral plans, and specific types of annuities. Additionally, certain exemptions for primary residences and assets with significant equity may apply, allowing individuals to maintain a degree of financial stability while still obtaining necessary care.

How Can Families Coordinate Medicaid Planning With Traditional Estate Plans?

Coordinating Medicaid planning with traditional estate plans requires a comprehensive approach that considers the goals of both strategies. Families should assess their asset structure, potential long-term care needs, and the implications of each planning method. Working with knowledgeable estate planning and Medicaid lawyers can ensure that both aspects are integrated seamlessly, maximizing benefits and protection for all family members.

Authored by Michelle A. Berglund-Harper, Esq., a member of The Florida Bar, Partner at Murphy & Berglund, PLLC since 2012. A link to the author’s bio can be found here.